Croatian

Croatian Bulgarian

Bulgarian Chinese (Traditional)

Chinese (Traditional) Arabic

Arabic Sindhi

Sindhi Shona

Shona Scottish Gaelic

Scottish Gaelic Samoan

Samoan Pashto

Pashto Luxembourgish

Luxembourgish Kyrgyz

Kyrgyz Kurdish (Kurmanji)

Kurdish (Kurmanji) Hawaiian

Hawaiian Corsican

Corsican Amharic

Amharic Uzbek

Uzbek Tajik

Tajik Sundanese

Sundanese Sesotho

Sesotho Sinhala

Sinhala Malayalam

Malayalam Malagasy

Malagasy Kazakh

Kazakh Chichewa

Chichewa Myanmar (Burmese)

Myanmar (Burmese) Zulu

Zulu Yoruba

Yoruba Telugu

Telugu Tamil

Tamil Somali

Somali Punjabi

Punjabi Nepali

Nepali Mongolian

Mongolian Marathi

Marathi Maori

Maori Latin

Latin Lao

Lao Khmer

Khmer Kannada

Kannada Javanese

Javanese Igbo

Igbo Hmong

Hmong Hausa

Hausa Esperanto

Esperanto Cebuano

Cebuano Bosnian

Bosnian Bengali

Bengali Urdu

Urdu Haitian Creole

Haitian Creole Georgian

Georgian Basque

Basque Azerbaijani

Azerbaijani Armenian

Armenian Yiddish

Yiddish Macedonian

Macedonian Icelandic

Icelandic Belarusian

Belarusian Welsh

Welsh Irish

Irish Swahili

Swahili Malay

Malay Afrikaans

Afrikaans Persian

Persian Turkish

Turkish Thai

Thai Maltese

Maltese Hungarian

Hungarian Galician

Galician Estonian

Estonian Albanian

Albanian Vietnamese

Vietnamese Ukrainian

Ukrainian Slovenian

Slovenian Slovak

Slovak Serbian

Serbian Lithuanian

Lithuanian Latvian

Latvian Indonesian

Indonesian Hebrew

Hebrew Filipino

Filipino Catalan

Catalan Swedish

Swedish Spanish

Spanish Russian

Russian Romanian

Romanian Portuguese

Portuguese Polish

Polish Norwegian

Norwegian Korean

Korean Japanese

Japanese Italian

Italian Hindi

Hindi Greek

Greek German

German French

French Finnish

Finnish Czech

Czech Danish

Danish Dutch

DutchService hotline

+86 0755-83975897

en

en

Release date:2021-12-29Author source:KinghelmViews:2348

As one of the three foundations of information technology, sensor technology is a high-tech developed by countries all over the world.

In recent years, the global sensor market has maintained rapid growth. With the continuous improvement of the economic environment and the continuous maturity of emerging technologies, the market demand for sensors is increasing.

According to the data of CCID Industrial Research Institute, in 2019, the global sensor market reached [敏感词] $152.11 billion, a year-on-year increase of 9.2%; China's sensor market reached 218.88 billion yuan, a year-on-year increase of 12.7%. The growth rate of the world and China has slowed down, but the growth rate of the domestic market is still higher than that of the world.

Despite the huge scale of China's sensor market, Germany, Japan, the United States and other countries are still active in the sensor market. In contrast, the development of China's sensor industry is slow, and more than 80% of sensors rely on imports.

Bu Rixin, partner of chuangdao capital, said:

From the perspective of industrial chain, China does not lack Internet of things application scenarios or network transmission equipment, but the bottleneck lies in the sensor end.Despite the policy support for many years, China's sensor industry is indeed in a relatively backward state, especially in terms of performance parameters such as accuracy and power consumption, there is a large gap with foreign products.

And non network introduced the industry layout, future innovation, opportunities and challenges of sensor manufacturers at home and abroad in previous special activities. Based on this, combined with the interview contents of industry institutions and investment institutions, sort out the development status of key products in the sensor industry, the direction of industry innovation, and the opportunities and challenges of domestic enterprises.

The highlight of the sensor industry

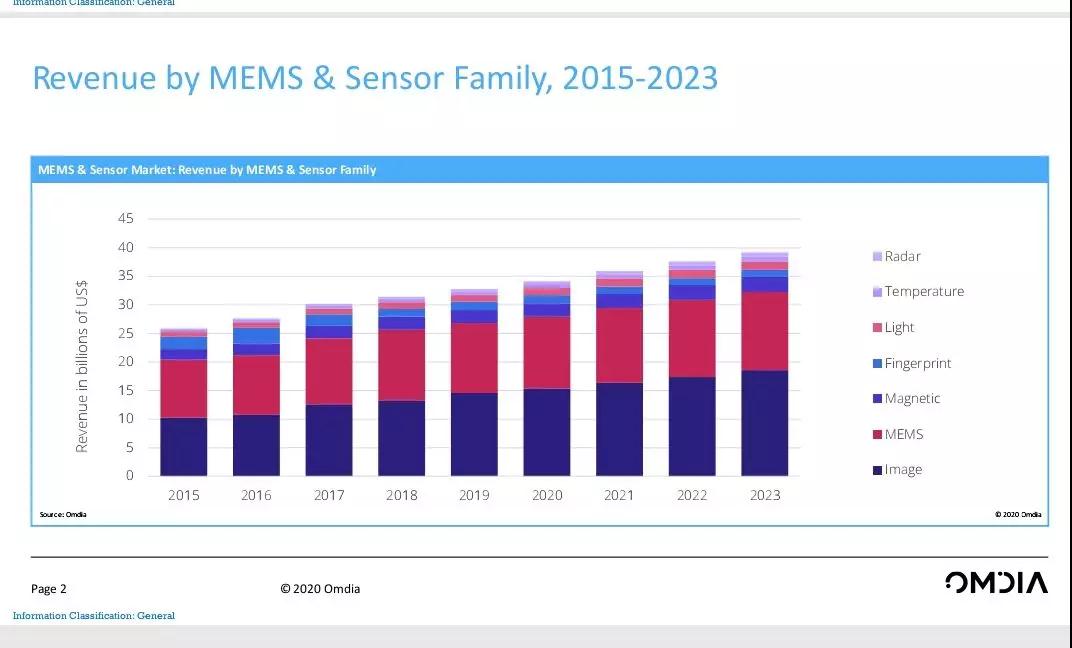

By function, sensors can be divided into image, MEMS, fingerprint, magnetic field, temperature and other categories. Among them, image and MEMS sensors are the absolute protagonists, and their sales are more than 4 times that of other sensors.

As for the growth trend of the protagonist, Manuel Tagliavini, senior analyst of IHS, said that the growth trend of the image sensor market was the strongest. On the contrary, the current scale dominated MEMS field has an irrational upward trend. It is expected that by 2023, the scale of image sensors can surpass the MEMS market.

MEMS sensor

In 2019, China's MEMS sensor market reached 59.78 billion yuan, a year-on-year increase of 18.3%.

MEMS sensors are mainly used in the consumer electronics market represented by mobile phones, and another important market is automotive electronics; The Asia Pacific region is undoubtedly the second largest sensor market after the North [敏感词]n market, and China is undoubtedly the fastest growing sensor market in the Asia Pacific region.

It can be seen that in recent years, with the rapid development of downstream industries such as consumer electronics and automotive electronic products, and the gradual transfer of the global electronic machine industry and hardware innovation market to China, the demand growth of MEMS devices in the Chinese market is much higher than that of the global MEMS market.

Although the domestic demand is large, the supply capacity is insufficient and the MEMS field is highly concentrated. Emerson, Siemens, Bosch, Italian French semiconductor, Honeywell and other multinational companies account for more than 60% of the market share, especially the products are almost completely supplied by imports, and 80% of the chips depend on foreign countries;

The remaining shares are mainly concentrated in several listed companies, such as goer acoustics, crystal optoelectronics, Hanwei electronics, Shilan micro and Jinlong Electromechanical, accounting for more than 40% of the domestic MEMS market; 70% of domestic MEMS enterprises are small and medium-sized enterprises, and their products are mainly concentrated in the middle and low end.

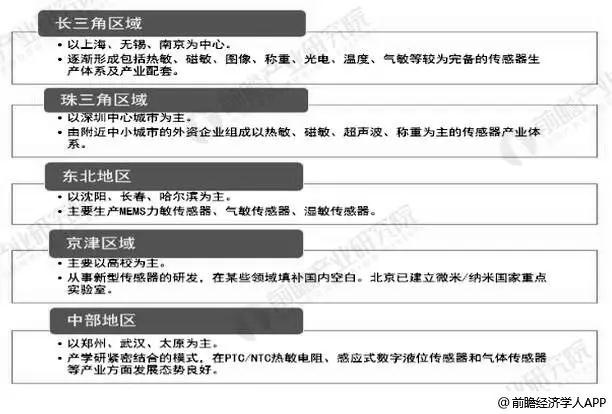

For China's MEMS sensor industry agglomeration area, the survey of prospective industry research institute shows that driven by industry demand and encouraged by national policies, China's MEMS industry has rapidly penetrated into the whole country, and a complete industry university research layout has been established in the Yangtze River Delta and Beijing Tianjin Hebei region.

From the perspective of enterprise distribution, it is mainly concentrated in the Yangtze River Delta, accounting for more than 50%, of which Jiangsu Province accounts for nearly 30%. This is due to the good foundation of integrated circuit industry in the Yangtze River Delta, more resources for silicon-based MEMS R & D and OEM production lines, complete industrial chain and key enterprises covering design, OEM and packaging and testing.

Under the background of good application prospect of MEMS sensors and accelerated localization process, there are broad prospects in the future. The data show that the average annual growth rate of China's MEMS sensor market will remain at about 15% in the next few years. It is predicted that China's MEMS sensor market will reach 148.86 billion yuan by 2025.

CMOS sensor

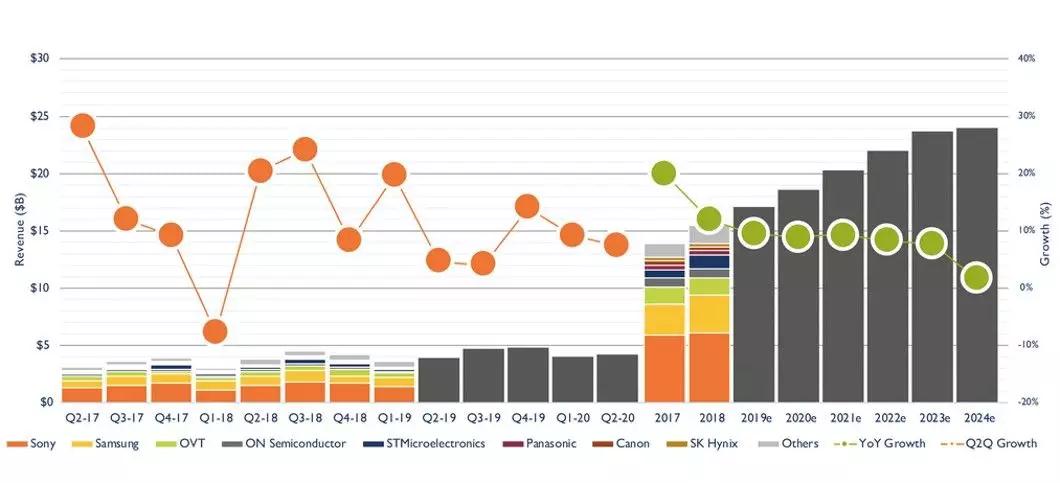

For CMOS image sensor (CIS), according to the data statistics of Xu Shaofu, an analyst of Jibang consulting, the global sales amount of CIS in 2019 was about [敏感词] $18.8 billion, a year-on-year increase of about 26%; The sales volume in China was [敏感词] $8.9 billion, a year-on-year increase of about 47%.

Yole Dé Forecast CIS market size by veloppement:The trend is similar in mid-2019

In terms of the overall market, driven by the trend of smart phone multi lens, CIS demand shows a high growth; In addition to the huge domestic demand market, most module plants and EMS plants are concentrated in China, which is another reason for the high sales in China.

From the analysis of CIS terminal application requirements, consumer electronics is the largest application field of CIS at present. Among them, smart phones account for about 70%, with the highest share, and the multi lens trend is the main reason. Other application fields include automobile, security, wearable devices, industry, etc.

CarsElectronics

The popularity and penetration of ADAS system have attracted much attention in recent years, which has promoted the increase in the number of vehicle lenses and the introduction of high-resolution lenses, which have become another main source of demand for CIS in applications such as reverse development, automatic braking, landscape and in vehicle images.

Securitymonitor

Thanks to the promotion of domestic regional policies, a large number of security monitors were installed, and the growth increased steadily.

For example, for IP cam used in IOT, the products requiring camera modules have become the main products promoted by manufacturers. In addition, TV, smart audio, wearable devices and other products have also begun to carry camera modules, which is also the increasing demand for CIS in consumer imaging related applications.

Industrymanufacture

Machine vision application is the main factor driving the demand for CIS in this field. It drives the demand in image recognition, face recognition, optical detection and other functions.

From the perspective of global competition pattern, Sony, the leader of CIS industry, occupies more than 40% of the market share, focuses on the high-end market and has the strongest technical strength;

Under Sony is Samsung, which mainly focuses on the consumer electronics market. Most of them are self-produced and sold. They catch up with Sony in technology and can provide CMOS sensors of the same level as Sony, but Samsung has few industry-class applications.

Nowadays, more and more Chinese manufacturers are entering the market. Howell Technology (which has been acquired by Weill), Geke microelectronics, sitway, Ruixin micro and other local manufacturers cut into the market and seize the territory with their respective differentiation advantages.

Although there is still a certain gap between domestic CIS manufacturers and foreign manufacturers in terms of scale and technology, in the face of huge opportunities and bright prospects, some local manufacturers bravely meet the challenges and are gradually expanding their share and infiltrating into the medium and high-end market by relying on their own core technologies.

Challenges and breakdowns of local sensor industry

As the Internet of things enters the substantive development stage, the forward looking Industry Research Institute predicts that the global sensor market will maintain a growth rate of about 8% in the next five years, and the market scale will exceed [敏感词] $300 billion by 2024.

The view provided by IHS also shows that compared with AI and cloud computing, the Internet of things is the key driving force to really promote the development of the sensor industry.

New opportunities promote technological and application innovation, and innovation gives birth to new market opportunities. The two go hand in hand. With regard to the innovation direction of sensors, industry institutions and manufacturers expressed their respective views:

Compared with developed countries, local advantages are mainly in the application of downstream Internet of things, mode innovation and grasp of diversified market demand. In recent years, with the application of fingerprint, image and sound sensors, excellent sensor enterprises such as gekewei, Howe technology, goer shares and huiding technology have been born.

However, in addition to the market and application advantages, the deficiencies and defects of the local sensor industry are also obvious.

In the field of consumer sensors, there is little difference between domestic and foreign technology, but it involves traditional fields such as industry and automobile application. The domestic accumulation is relatively weak, the technical capacity is backward, and there is a large gap between the overall technical level and foreign countries.

In addition, there is a serious shortage of MEMS, CMOS and other products. The high-end sensors required by national major equipment still rely on imports, and the products of foreign-funded enterprises occupy the vast majority of the market share of the domestic high-end market.

Here, Lu Xiaobao, investment director of Zhongke Chuangsheng, shared the following views on the challenges faced by local enterprises:

workmanshipweakSemiconductor sensors, including MEMS sensors, are more process than design. Most domestic process lines have been gradually established in recent years, and experienced R & D personnel are relatively scarce;

MaterialsBasicsThe core of most sensors is often materials. Without the support of core materials, we cannot make the most advanced sensor products. There is a significant gap between China and leading countries such as Japan, Europe and the United States in terms of core materials;

Mass productionabilitySensors are often customized testing, many of which cannot be fully automatic. The domestic accumulation here is poor, and the quality control ability is weak;

According to the development suggestions of the current situation of the industry, the author interviewed many industry institutions:

Catalyst for sensor industry - Kechuang board

In the context of Sino [敏感词] trade war and domestic substitution, the launch of the science and innovation board is conducive to the development and growth of the whole science and technology industry. Excellent enterprises can quickly stand out, and mediocre enterprises gradually fall down, accelerating the trend of "survival of the fittest".

As the main participants in the capital market, industry investment institutions shared their significance and impact on the industry.

Zhongke Chuangxing said that with the national supply side structural adjustment, innovation driven development has become the mainstream. In fact, innovation driven also includes the innovation and further upgrading of science and technology enterprises. It is necessary to encourage and drive science and technology enterprises to develop in the direction of deep innovation and hard science and technology, rather than fighting in the low-end science and technology field.

On the whole, the launch of the science and innovation board is conducive to supporting the strong and retreating the weak in the industry, making the excellent bigger and stronger, and gradually weakening the mediocre, so as to finally form a relatively benign industrial pattern in which large enterprises have sufficient strength to fully participate in international competition, medium-sized enterprises have strong competitiveness in some segments, small enterprises continue to innovate, and weak enterprises can not survive being eliminated.

Through observation, it is very obvious that funds have poured into the field of science and technology, especially the field of semiconductors, in the past two years. Many people who didn't know anything about the semiconductor field are also entering the semiconductor field, but the actual situation is still not popular.

Frankly speaking, many enterprises focusing on the medium and low-end market do not have a strong spirit of innovation. To be competitive on a global scale, one is to rely on core technology, the other is to constantly innovate to guide new needs, and the third is to have good management efficiency without any other path.

The science and innovation board is opening rapidly. After some enterprises are listed, they gather more resources and are easier to expand. However, we hope that not only enterprises will become bigger, but also eventually become stronger.

Therefore, it is also recommended that investment institutions not only look at semiconductor themes and short-term sales, but also invest more resources in enterprises that really master core technologies and have better operation efficiency.

Then, with the addition of the science and innovation board, will the competition between the corresponding investment institutions become more intense? Bu Rixin doesn't think there will be particularly obvious wrestling or competition. Even if there is, it is temporary. The market will eventually mature and enter a virtuous circle.

Of course, the competition among investment institutions will gradually shift from the competition in capital to the competition in industry judgment and technical analysis. The investment institutions in the field of science and innovation will also be "technical" and "professional" investment institutions.

Write at the end

Message sensor start-up

Then, with the gradual maturity of the sensor industry and application market, do start-ups still have opportunities and ways to enter the market? Industry investment institutions replied to the author on this issue.

It can be seen that barriers to the sensor industry have already appeared, the window period is narrowing rapidly, and entrepreneurial opportunities are decreasing. In addition, the launch of scientific innovation board is like a straw for new enterprises.

It is the life-saving straw for enterprises to "find the right market segments, grasp the differentiated demand and win the favor of the capital market";

It is also the last straw for overcoming the "blind approach, the pursuit of heat and the neglect of bubbles".

This article is reproduced from“And non network”, support the protection of intellectual property rights. Please indicate the original source and author for reprint. If there is infringement, please contact us to delete

Copyright © Shenzhen Kinghelm Electronics Co., Ltd. all rights reservedYue ICP Bei No. 17113853